If my company offers interest-bearing intra-group loans, is it in- or out-scope of the economic substance law?

This article explores one particular consideration in this topic, which is the interpretation of whether an entity is carrying out finance and leasing business, and specifically, whether providing interest-bearing intra-group financing qualifies as finance and leasing business in the BVI.

A helpful premise to start off the discussion is this: if your entity offers short-term credit as an incidental part of its usual operations, it is ruled out of being a finance and leasing business. The confusion, however, arises when considering whether any interest-bearing loan brings an entity into scope of requiring substance in the jurisdiction, or whether the loan issued is incidental to the main business of the entity, and if this then impacts its substance classification.

Our view is that while neither the Act nor the Rules explicitly defines intra-group loans as being either in or out of scope as a finance and leasing business, an argument could be made that if a loan is made to a subsidiary, it should then be considered incidental to the actual purpose and nature of the entity’s business activities. Accordingly, the entity would not be considered as a finance and leasing business. The example below illustrates why.

Case study

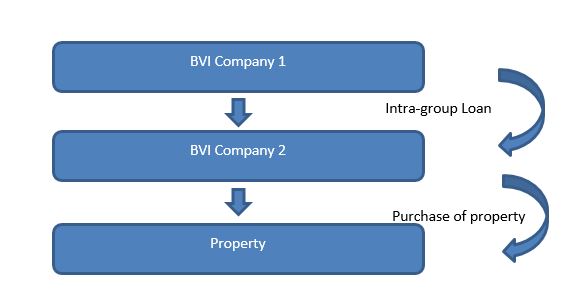

As the following diagram shows, BVI Company 1 was set up to hold the equity of BVI Company 2, which was in turn used to purchase a property.

In order to purchase the property, BVI Company 1 makes a one-off loan to BVI Company 2 for the value of the property at an interest rate to cover the cost of the external borrowing it has received from a third-party bank.

Given such, the directors of BVI Company 1 can then conclude that Company 1 is carrying out a holding business only (subject to it meeting the narrow criteria of that relevant activity), and not a finance and leasing business, because the loan was incidental to the principal business of BVI Company 1.

Therefore, unless an entity has been providing loan financing to subsidiaries or third-parties frequently or as its main business, it is possible to argue that the entity does not carry out finance and leasing business in all cases, but this is very dependent on the nature and relative size and objective of the financing*.

As a side issue, for the Crown Dependencies of Jersey, Guernsey and the Isle of Man, their guidance states that intra-group loans are clearly in scope, and thus the argument concerning the incidental nature of a loan becomes less prominent. This means that more entities will fall into the category of finance and leasing business in these jurisdictions. Whether the European Union plans to seek consistency across jurisdictions remains to be seen, and thus the situation may be uncertain for months to come.

Key takeaway

So what does all of this mean for businesses with structures in the BVI, Cayman Islands and other jurisdictions?

The key takeaway is to understand that each entity must be reviewed and classified on its own merits, and that full consideration should be given to all the activities of the entity and the jurisdiction in which it is resident. Equally important, directors of an entity must be able to demonstrate this consideration and articulate the thought process of the incidental nature of the financing upon request for any audit by authorities.

At this critical juncture, we encourage you to reach out and understand how you can ensure substance compliance in the BVI. Please contact your Account Manager or fill in the enquiry form here to find out more about how we can help.

*A caveat to note is that if the terms and interest of the loan go beyond or far exceed the terms of the loan extended by the third-party bank, it could then be argued that the loan is not incidental to the entity’s business, and would therefore constitute finance and leasing business.

The contents of this article are intended for informational purposes only. The article should not be relied on as legal or other professional advice. Neither Vistra Group Holding S.A. nor any of its group companies, subsidiaries or affiliates accept responsibility for any loss occasioned by actions taken or refrained from as a result of reading or otherwise consuming this article. For details, read our Legal and Regulatory notice at: https://www.vistra.com/notices . Copyright © 2024 by Vistra Group Holdings SA. All Rights Reserved.